Key Points

- GMX is a self-custody perp DEX for spot swaps, long/short positions, and leveraged crypto trading.

- The strongest fit is experienced DeFi traders, active LPs, and users already comfortable with wallet-based execution.

- GMX uses oracle pricing, GM pools, and GLV pools rather than a traditional order book.

- Core risks include liquidation, smart contract risk, ADL, funding costs, and LP exposure.

Overview

GMX is a decentralized exchange for spot swaps and perpetual futures trading. Users connect a wallet, choose a market, select collateral, and trade directly from self-custody. Readers researching broader market context can compare GMX with MarketBit coverage on crypto market research and the exchange review hub.

GMX runs across major DeFi ecosystems, with Arbitrum and Avalanche playing central roles in liquidity and user activity. For live access, users can visit the GMX official site or open the GMX trading app. Market data from the DefiLlama GMX page showed about $429.75 million TVL, $304.06 billion cumulative perp volume, $119.35 million open interest, $7.67 billion 30-day perp volume, and $5.02 million 30-day fees as of May 19, 2026.

| Metric | GMX Snapshot |

| TVL | ~$429.75M |

| Cumulative perp volume | ~$304.06B |

| 30-day perp volume | ~$7.67B |

| Open interest | ~$119.35M |

| 30-day fees | ~$5.02M |

| Main liquidity hub | Arbitrum |

| Max leverage | Up to 100x |

Key Features

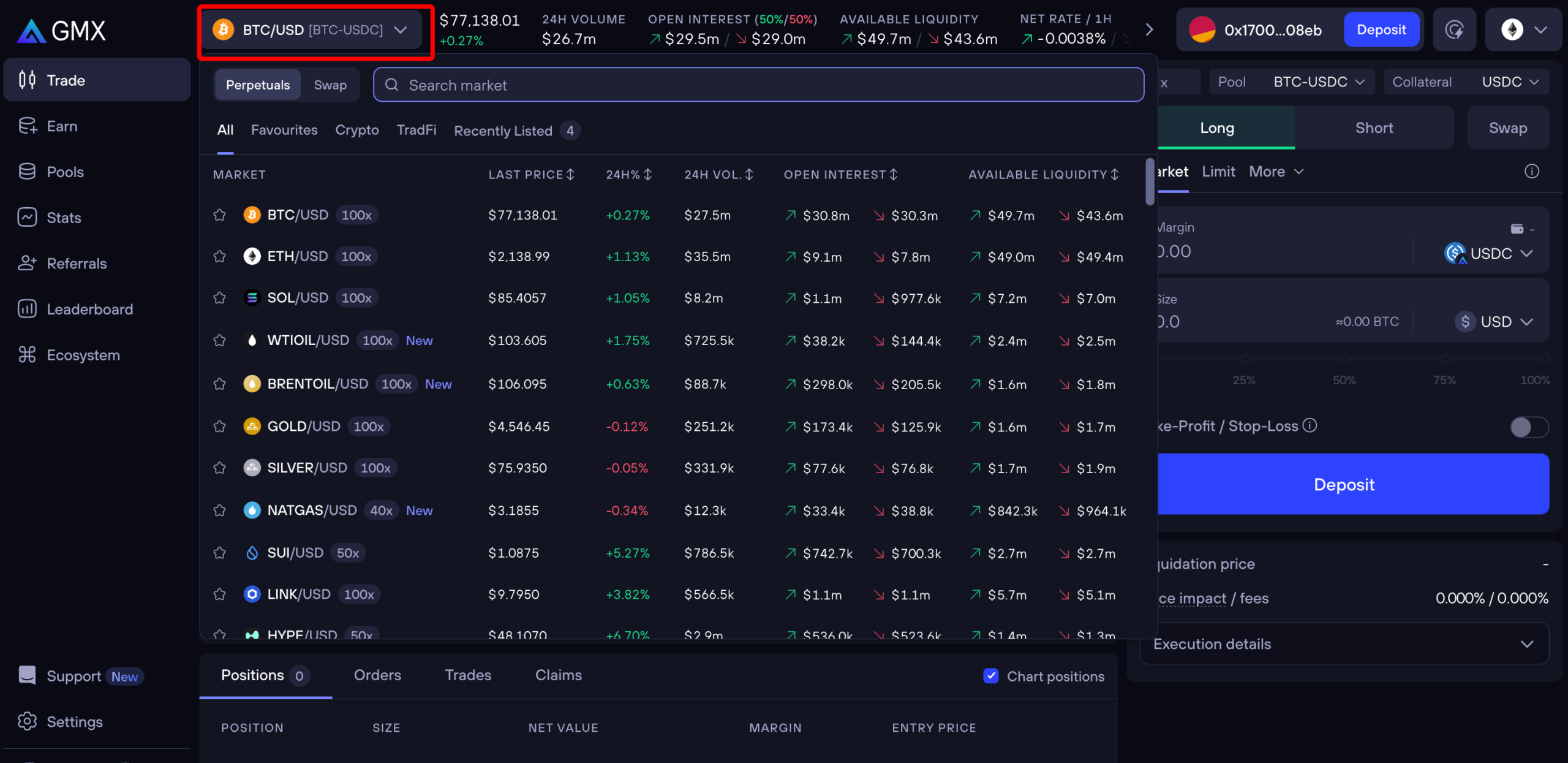

GMX core product is perpetual trading. Traders can open long or short positions, adjust leverage, manage collateral, and close exposure without moving funds into a centralized venue. MarketBit’s perpetual futures analysis adds useful background for readers comparing GMX against order-book venues.

The market screen is practical. A search bar helps users locate pairs quickly, while category filters reduce scanning time when liquidity expands across more assets. For active users, a cleaner market discovery flow matters because wrong-pair selection or thin-market execution can increase trading mistakes.

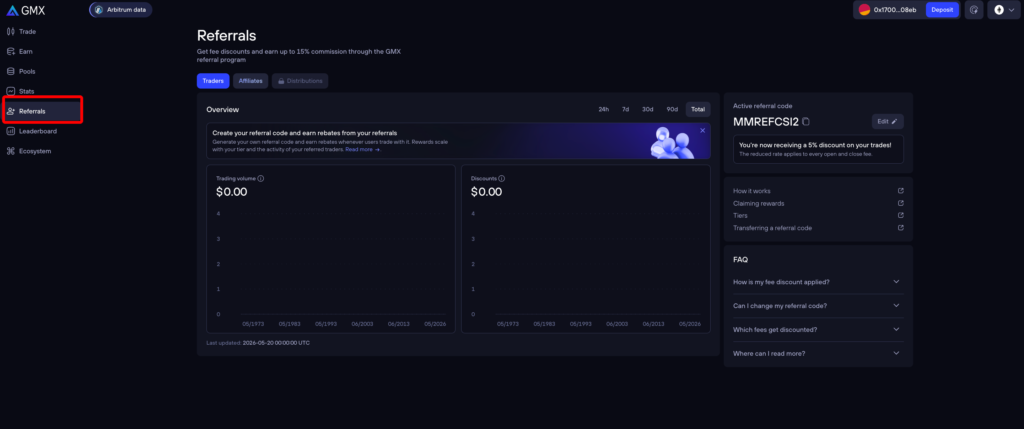

GMX also supports referrals. Traders can receive fee discounts, while affiliates can earn commission from referred trading activity. The feature gives GMX a growth loop common in centralized exchanges, but still keeps trading tied to wallet-based execution.

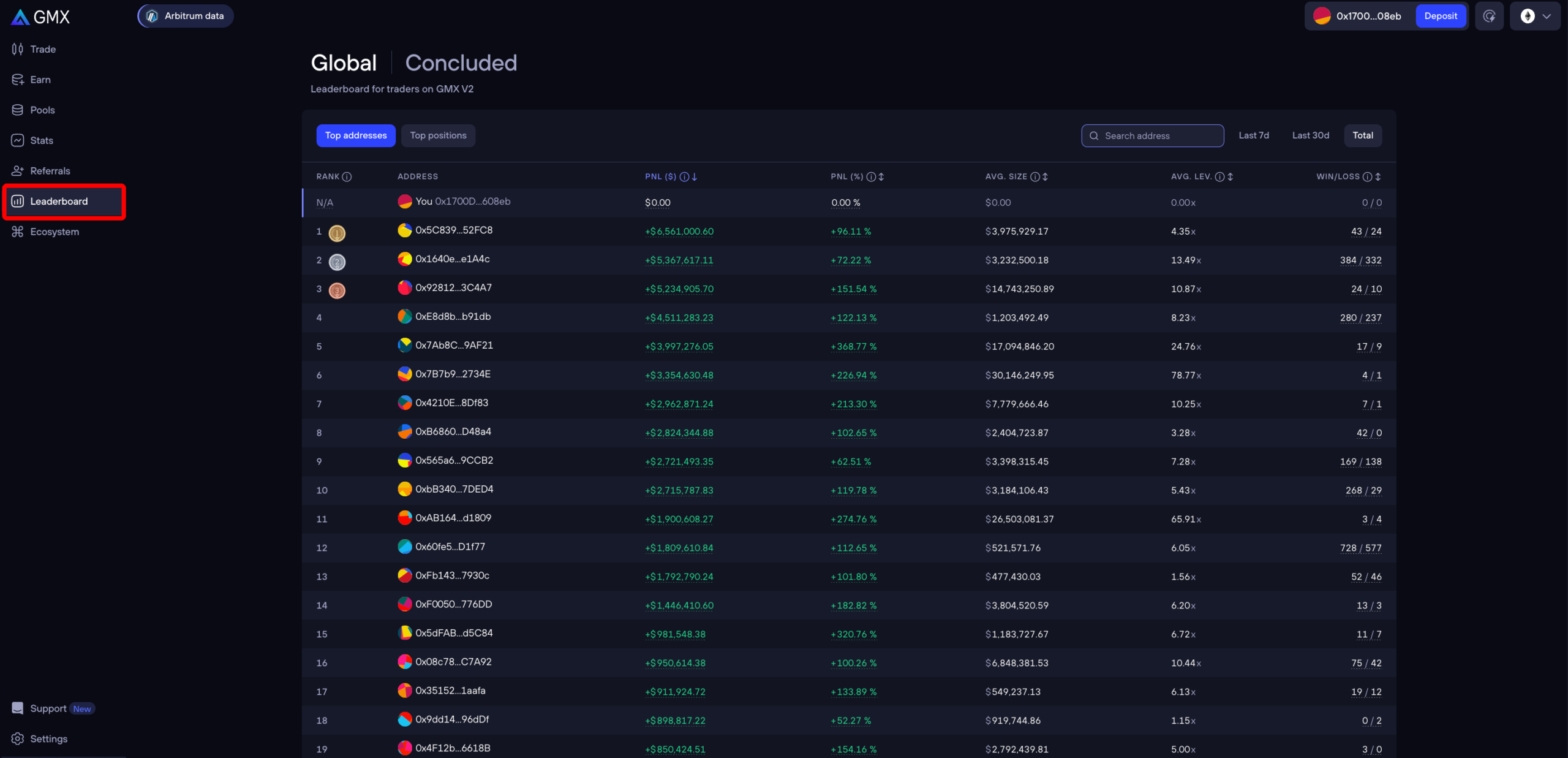

The leaderboard adds a social proof layer. It ranks traders based on realized profits, which helps readers see active participation beyond protocol-level volume. Leaderboard data should still be treated carefully because high realized profit never removes liquidation risk or strategy risk.

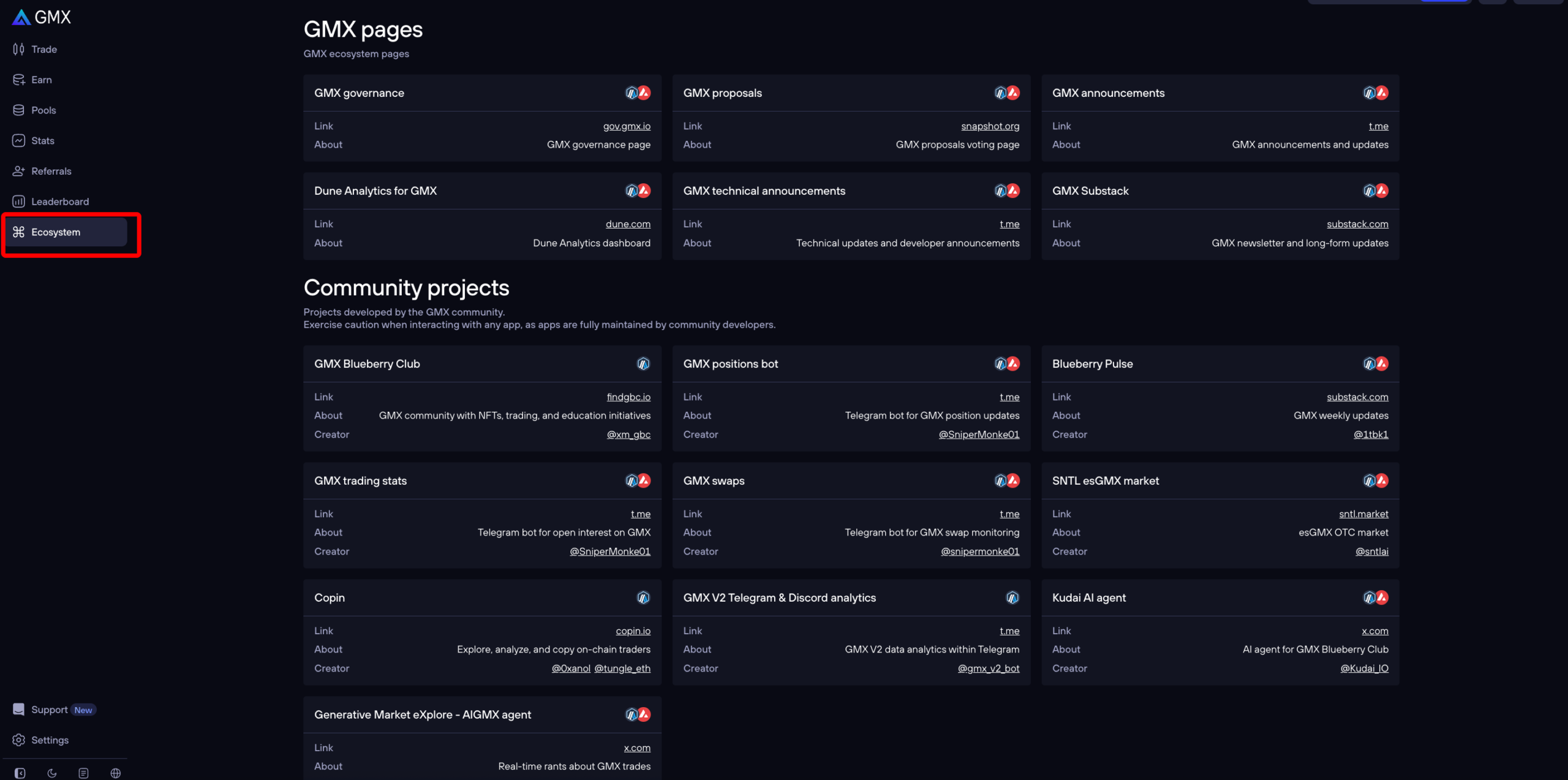

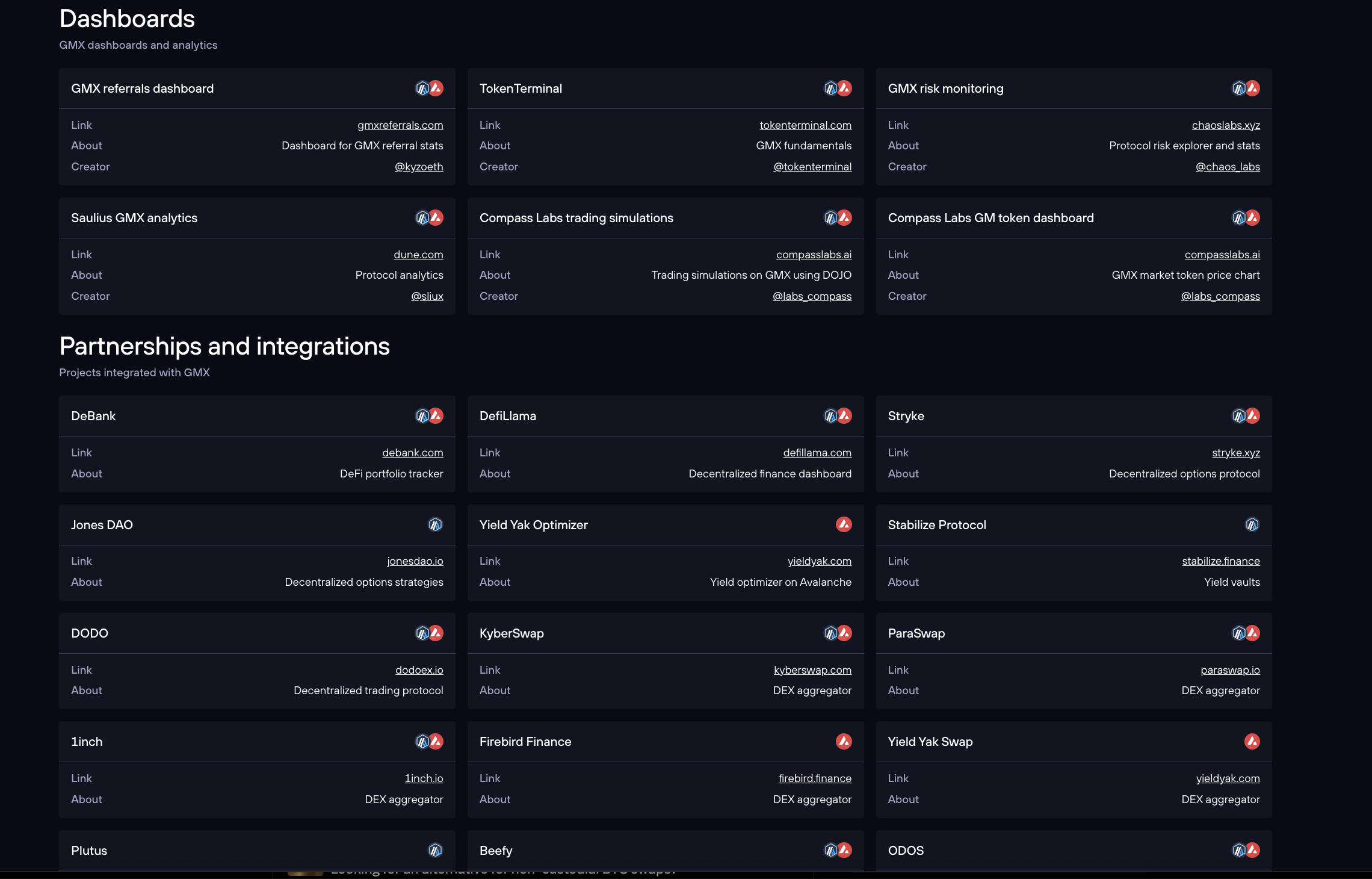

The pages hub groups official resources, dashboards, community tools, and partner integrations. For a trader, the hub helps locate research and execution tools. For an LP, the hub helps locate analytics needed before selecting GM or GLV exposure.

The dashboard and integration area rounds out the product. GMX is not only a trade panel; it also offers a data layer for monitoring pools, trading flow, and ecosystem links.

How GMX Works

GMX uses a pool-backed trading model. Instead of matching buyers and sellers through an order book, trades interact with liquidity pools. Pricing relies on external market feeds such as Chainlink Data Streams, while liquidity comes from GM pools and GLV pools.

GM pools are market-specific liquidity pools. GLV pools are broader vault-style pools designed for allocation across supported markets. Liquidity providers earn a share of trading activity, but they also absorb market risk, trader profit-and-loss exposure, and pool imbalance risk.

| Category | GMX Pool Model | Order-Book Exchange |

| Execution | Against liquidity pools | Against buyers and sellers |

| Pricing | Oracle-based pricing | Bid/ask order book |

| Liquidity source | LP deposits | Traders and market makers |

| Custody | Wallet-based self-custody | Usually exchange custody |

| Main advantage | Transparent DeFi execution | Speed and deep centralized liquidity |

| Main weakness | More complex risk model | Custody and platform risk |

Fees

GMX fees are dynamic. The main position fee for many crypto markets is usually 0.04% or 0.06%, depending on whether a trade improves or worsens market balance. Users should also study gas conditions on Arbitrum and Avalanche because network cost can affect smaller trades.

| Fee Type | Explanation |

| Position fee | Charged when opening, closing, increasing, or reducing a position |

| Swap fee | Dynamic fee based on pool balance impact |

| Borrowing fee | Paid over time when position demand uses pool liquidity |

| Funding fee | Transfers value between long and short sides |

| Network fee | Covers execution and gas-related costs |

| Price impact | Positive or negative adjustment based on pool balance |

| Liquidation fee | Charged when a position falls below required collateral |

A GMX trade cost is not only the headline position fee. Serious traders should review borrowing fees, funding fees, network costs, price impact, and liquidation distance before confirming any position.

User Experience

GMX feels more advanced than a simple swap app. The trading page shows charting, market selection, collateral, leverage, estimated fees, liquidation price, and execution details. The layout is familiar for perp traders, but beginners still need time to understand every field.

- Open the GMX app.

- Connect a wallet.

- Select network and market.

- Choose long or short.

- Set collateral and leverage.

- Review liquidation price, fees, and price impact.

- Confirm the trade.

The interface is clean, but GMX still expects users to understand DeFi basics. Wallet approvals, gas fees, collateral choice, and leverage management require more skill than a centralized exchange account.

My Experience Using GMX (Trader vs Liquidity Provider)

From a traders perspective, GMX works best after the user already knows the target market, position size, and invalidation level. The trade panel makes leverage, collateral, fees, and liquidation price visible before execution. Transparency is the strongest part of the trading flow, especially for users moving away from opaque centralized venues.

The trader workflow still demands discipline. A position can look affordable at entry, then become expensive when funding fees, borrowing fees, and price impact stack up. Stop-loss planning also needs room between liquidation distance and exit level.

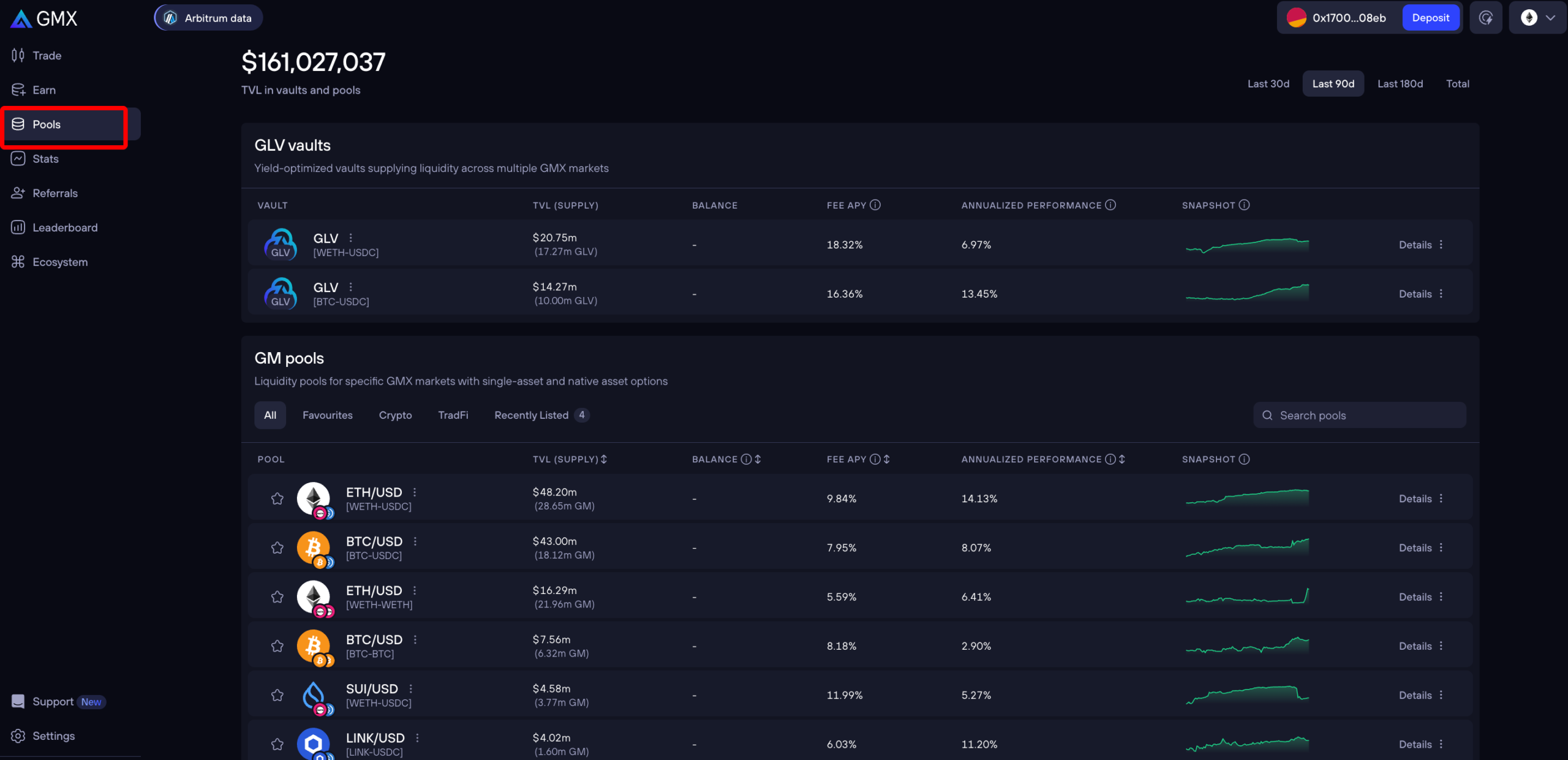

From a liquidity providers perspective, GMX feels like a separate product. The Earn page shows staking and pool choices, while GM and GLV areas make yield, liquidity, and exposure easier to compare. LPs should avoid reading headline yield alone; pool composition and trader PnL exposure matter more than a single return figure.

The GLV and GM pool views help LPs separate passive vault-style allocation from more active market-specific exposure. Passive does not mean risk-free. LP capital can gain from fees yet lose from asset moves, trader wins, or pool imbalance.

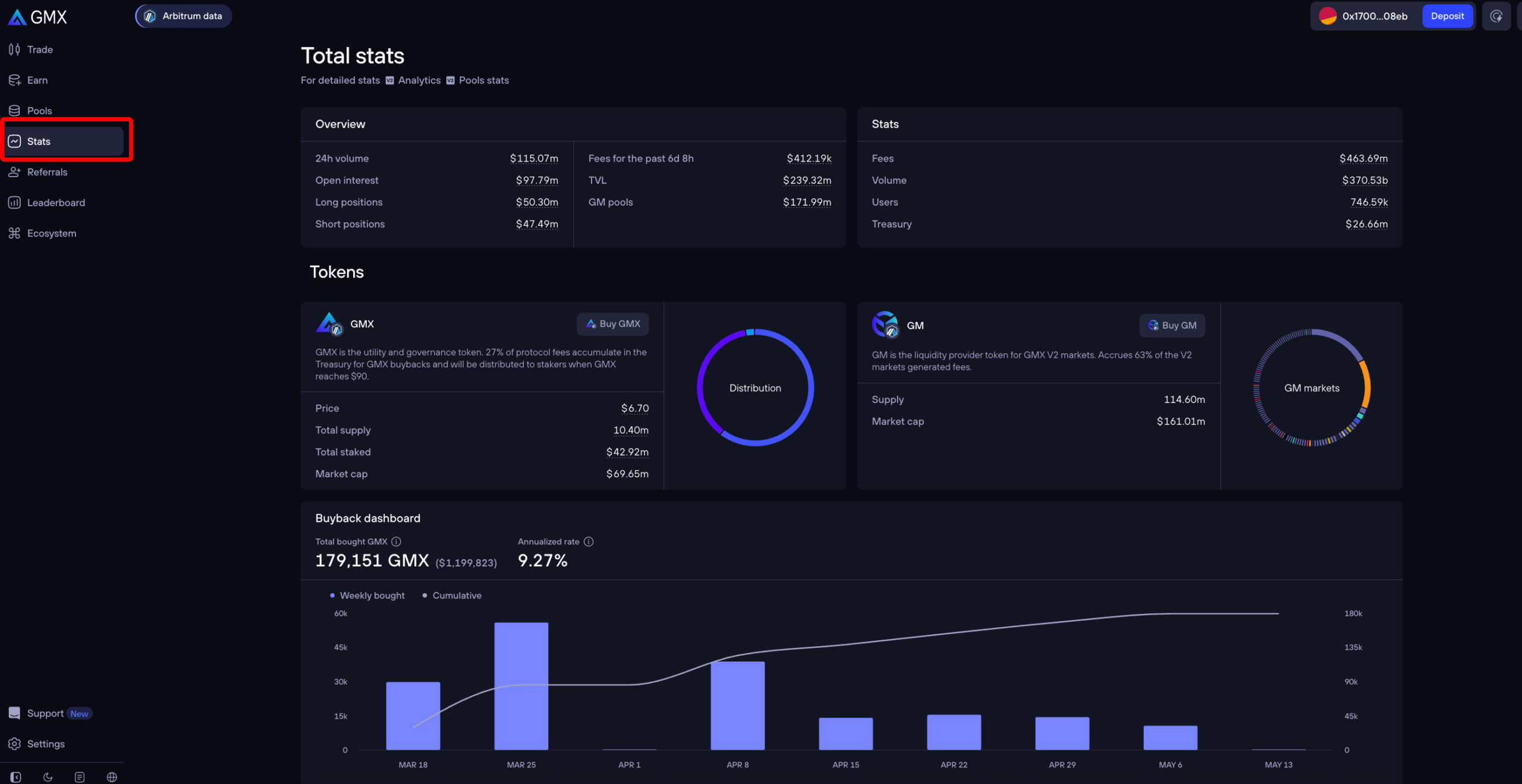

The analytics dashboard is valuable because it gives context beyond quoted APY. Volume, fees, utilization, pool value, and trader activity help reveal whether yield is supported by real usage. For LPs, analytics should come before capital allocation, not after.

The GM pools table is the most useful LP screen in the screenshot set. It shows market-specific opportunities, making it easier to compare pools by asset, liquidity, and yield. In my view, traders can use GMX after understanding the trade ticket, while LPs need a fuller research process before allocating capital.

| Role | Main Benefit | Main Risk |

| Trader | Self-custody leveraged exposure | Liquidation and fee drag |

| Liquidity Provider | Fee exposure from trading activity | Trader PnL and asset exposure |

| Active DeFi user | Transparent on-chain venue | Smart contract and wallet risk |

| Beginner | Clear interface helps learning | Product complexity remains high |

Security and Risks

GMX is non-custodial, so users keep control of wallet funds. Custody risk drops, but protocol risk remains. Users can inspect public code via GMX GitHub and review bounty coverage through GMX bug bounty on Immunefi.

Major risks include smart contract vulnerabilities, oracle assumptions, liquidation risk, stablecoin depeg risk, bridge risk, wallet compromise, and auto-deleveraging. One-click trading features may improve speed, but browser-based signing convenience requires careful wallet security.

Token and market researchers can also compare GMX on the CoinGecko GMX page and CoinMarketCap GMX page. Price pages are not risk analysis by themselves, but they help cross-check token liquidity, market cap, and exchange listings.

GMX Token

GMX token serves governance and ecosystem functions. The token is tied to protocol fee mechanics, including buyback activity funded by a portion of trading-related fees.

Token exposure should be analyzed separately from platform usage. A trader can use GMX without holding GMX token. An investor considering GMX token needs to evaluate revenue, governance, treasury policy, fee buybacks, token emissions, and broader market conditions.

Who Should Use GMX (Traders vs LPs)

| User Type | Fit | Reason |

| Active perp traders | Strong | Self-custody long/short trading with leverage |

| Advanced DeFi users | Strong | Comfortable with wallets, gas, collateral, and risk controls |

| Liquidity providers | Conditional | Fee opportunity exists, but pool exposure is complex |

| CEX-only users | Weak | No familiar account-based trading flow |

| Beginners | Weak | Leverage, liquidation, and DeFi mechanics create high risk |

GMX is best for users who understand DeFi execution, wallet security, perpetual contracts, and LP risk. It is not ideal for users seeking fiat deposits, customer support, or simple beginner onboarding.

Pros and Cons

| Pros | Cons |

| Self-custody trading | Not beginner-friendly |

| No traditional exchange account | Smart contract risk |

| Long and short positions | Liquidation risk |

| Up to 100x leverage | Dynamic fees require attention |

| GM and GLV liquidity options | LPs can lose when traders win |

| Transparent on-chain activity | Less convenient than CEX trading |

GMX vs Competitors

GMX competes with centralized exchanges and other perpetual DEXs. Its biggest difference is the liquidity pool model.

| Platform Type | Strength | Weakness |

| GMX | Self-custody, pool-backed perps, DeFi-native LP design | Complex risk and fee model |

| Order-book perp DEXs | Faster, familiar trading structure | Different decentralization tradeoffs |

| Centralized exchanges | Deep liquidity, fiat support, simple UX | Custody, KYC, and platform risk |

Centralized exchanges may offer faster execution and more markets. GMX offers stronger self-custody and on-chain transparency. For advanced users, the difference is not only product design; it is a question of control versus convenience.

Final Verdict

GMX remains one of the most important decentralized perpetual exchanges in 2026. It is a serious venue for experienced traders who want wallet-native leverage, transparent execution, and on-chain market access.

For liquidity providers, GMX can offer meaningful fee exposure, but LP participation should never be treated as passive yield without risk. Pool composition, trader profits, utilization, volatility, and asset exposure all matter.

GMX is worth using for advanced DeFi traders and LPs who understand the mechanics. It is not a simple replacement for centralized exchanges, and beginners should study leverage, liquidation, and wallet security before trading with real size.

FAQs

Is GMX safe to use?

GMX is non-custodial, which reduces exchange custody risk. Users still face smart contract risk, oracle risk, liquidation risk, and wallet security risk.

Does GMX require KYC?

GMX does not use a traditional centralized account flow. Users connect a wallet and trade on-chain. Local rules may still apply depending on user location.

Can beginners use GMX?

Beginners can access GMX, but the platform is better suited for experienced users. Leverage, collateral, liquidation, and DeFi wallet management can be difficult for new traders.

Is GMX better for traders or liquidity providers?

GMX can serve both groups. Traders get self-custody perpetual trading, while liquidity providers get fee exposure through GM and GLV pools. Risk profiles are completely different.